4 People Who Should Stop Before Making the Retirement Move

- admin469378

- Feb 4

- 6 min read

Updated: Apr 9

Most people want to retire due to exhaustion of the daily grind.

But, here’s the part that surprises many people:

the transition into retirement can be more disruptive—emotionally, psychologically, and physically—than they expect.

Research shows that in the first year after retirement, the risk of a heart attack or stroke increases dramatically compared to peers who are still working.

Study Link Here: Transition to retirement and risk of cardiovascular disease: Prospective analysis of the US Health and Retirement Study - PMC

This isn’t because retirement itself is harmful, and it’s not because people suddenly run out of money.

It's because abrupt life transitions matter more than we give them credit for.

As a fiduciary financial planner at Parkmount Financial, I see this intersection of money, health, and behavior every day.

Retirement isn’t just a financial event—it’s a human one.

And that’s why there are certain types of retirees who benefit from pausing before stepping away from work.

If you’re thinking about retiring soon, start with a simple step:

👉 Schedule a free financial consultation to pressure test both the numbers and the lifestyle changes.

If you find yourself in one of the following categories, you may benefit from a retirement re-assessment.

1. The Identity-Dependent Retiree

These are often high-functioning professionals. Their work provides structure, relevance, social interaction, and a sense that they matter.

Then retirement arrives—and all of that disappears at once.

At first, things feel great.

There may be a honeymoon phase filled with travel, home projects, or long-delayed hobbies. But for many people, that initial excitement fades quickly, leaving the retiree disoriented.

Work gives the nervous system rhythm: wake times, expectations, social engagement, and a reason to show up. When that rhythm disappears overnight, the body often doesn’t respond with calm—it can feel like anxiety and emptiness.

Behavioral research on retirement transitions highlights how involuntary retirement or loss of meaning at work correlates with declines in mental health and well-being for certain individuals.

More details on the study here: https://pubmed.ncbi.nlm.nih.gov/41369789/

Behavioral Finance Insight

From a behavioral finance perspective, this is a classic case of underestimating

non-financial risk. People plan carefully for market volatility but overlook identity loss, routine disruption, and social withdrawal.

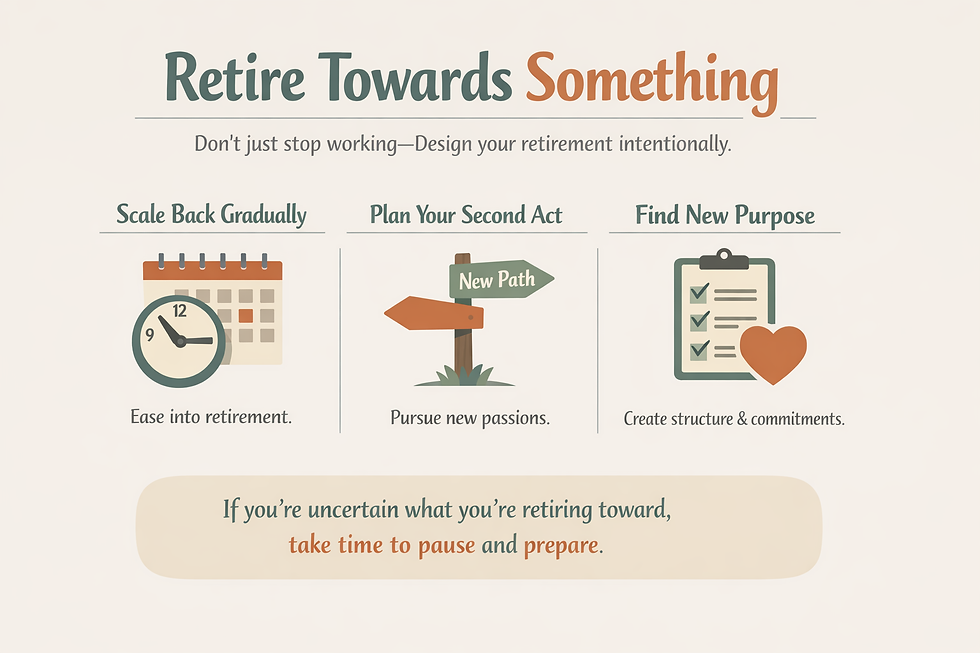

The Fix: Retire Towards Something

The solution isn’t to work forever. It’s to design retirement intentionally.

That might mean:

Scaling back instead of stopping abruptly

Designing a second act before your last day of work

Creating structure and commitments that replace what work once provided

If you’re unsure what you’re retiring toward, that’s not a failure—it’s a signal to pause and prepare.

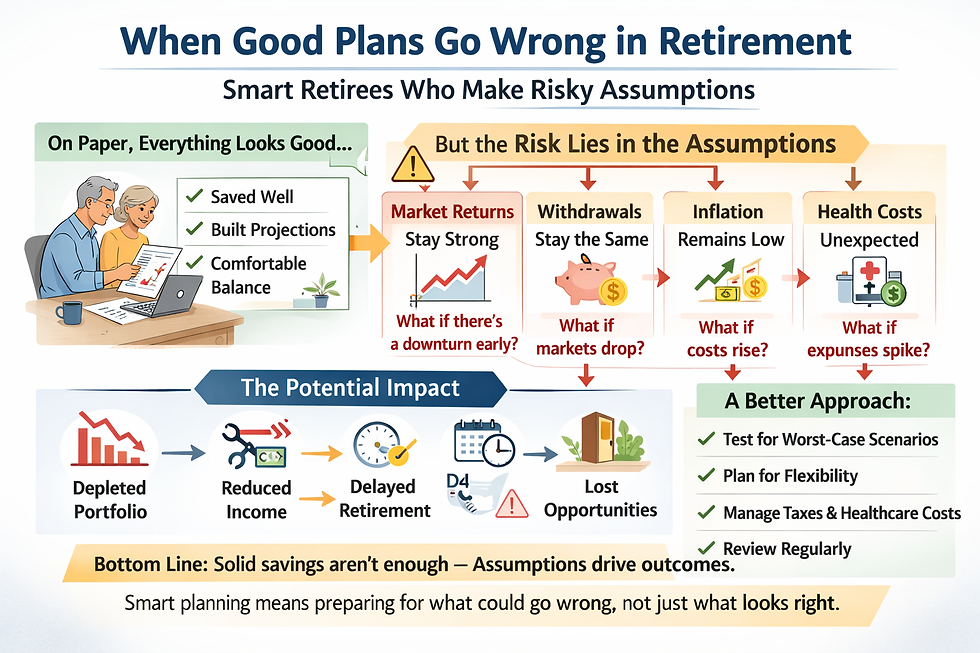

2. The Spreadsheet Surfer Retiree

The second group is the spreadsheet surfer retiree. These are analytical people who’ve saved well and built their own retirement projections.

On paper, everything looks solid.

But the risk lies in the assumptions.

I recently met with a highly compensated professional who had created his own retirement spreadsheet. He projected a 10% annual return, held a portfolio heavily concentrated in stocks, and planned to retire within two years.

The math wasn’t wildly wrong—but it was fragile.

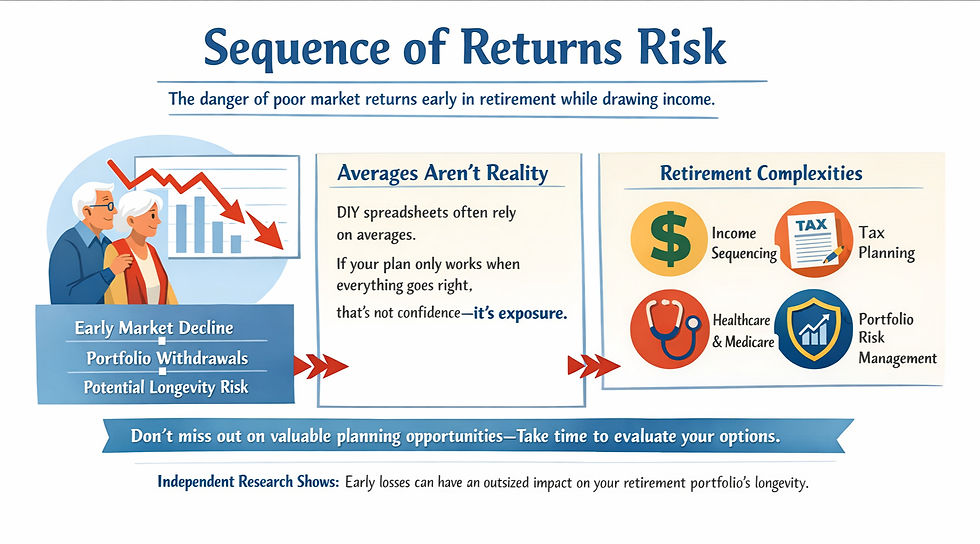

Sequence of Returns Risk

One of the most underestimated risks in retirement planning is sequence of returns risk—the danger of experiencing poor market returns early in retirement while simultaneously drawing income.

Independent retirement research on sequence of retirement portfolio returns and timing risk explains why early market downturns can have outsized impacts on portfolio longevity.

Researchers at MIT Wrote a Research Report on It Here: https://mitsloan.mit.edu/action-learning/mitigating-sequence-returns-risk-sorr

DIY spreadsheets often rely on averages. If your plan only works when everything goes right, that’s not confidence—it’s exposure.

In addition, Retirement introduces new complexities like income sequencing, tax planning, healthcare and Medicare decisions, and portfolio risk management, to name a few.

At the very least, if relatively in a low risk, well-funded position, they could be missing out on significant planning opportunities which are worth pausing to evaluate.

The Fix: Stress‑Test, Don’t Guess

A prudent retirement plan stress‑tests assumptions, builds buffers, and prepares for unfavorable early outcomes—not just average ones.

3. The Lifestyle Drift Retiree

The third group is the lifestyle drift retiree, which I see often in high‑income households.

Strong earnings can hide weak habits. People save substantial amounts but never clearly define what their lifestyle actually costs.

One physician described watching peers earn hundreds of thousands of dollars—sometimes more—and still live paycheck to paycheck.

High income can mask risk.

Why Spending Awareness Matters

Retirement doesn’t start with assets. It starts with expenses.

If you don’t know what you spend—you can’t know whether retirement is sustainable. Net worth alone doesn’t determine readiness.

While spending patterns in retirement vary, economic research on retirement consumption trends and spending behavior shows that retiree spending does not always follow simple assumptions and may change in complex ways during the retirement transition.

More research on the spending trends by age can be found here: https://www.sciencedirect.com/science/article/abs/pii/S0047272724000392

Behaviorally, spending tends to drift upward over time with income. In retirement, there’s no paycheck to correct mistakes and much less wiggle room for error to cover for bad habits.

In Retirement, every dollar out must be supported by a plan, and if distributions are excessive, that could mean risk of running out of money way too soon, and faster than people think.

This disconnect often leads to people feeling wealthy on paper but anxious in real life.

The Fix: Clarity, Not Restriction

The goal isn’t deprivation. It’s awareness.

When spending aligns with values, confidence follows.

4. The “Still‑In‑It” Retiree

The most surprising group is the still‑in‑it retiree.

This person may be financially ready. The numbers work. The resources support the lifestyle. But they still enjoy their work.

They feel useful, engaged, and energized—yet feel pressure to retire because it’s what they’re “supposed” to do.

For this group, retiring too early can create a vacuum rather than freedom.

Retirement Isn’t Binary

Retirement doesn’t have to be all‑or‑nothing. Sometimes scaling back hours or shifting roles preserves purpose while improving balance.

From a planning standpoint, these retirees may even be overfunded. That’s not a problem—it simply shifts the focus toward tax efficiency, legacy planning, and aspirational goals.

The Fix: Let Work Be Information

If work still contributes positively to your life, that’s not a flaw—it’s insight.

Retiring Well vs. Retiring Fast

The goal of retirement planning isn’t to exit work as quickly as possible. It’s to retire well.

That often means slowing down and ensuring that your plan supports your health, identity, and peace of mind—not just your balance sheet.

If you’d like help stress‑testing your retirement strategy, Parkmount Financial offers a complimentary consultation designed to provide clarity—not sales pressure.

SCHEDULE HERE👉 https://www.parkmountfinancial.com/free-consultation

Disclosures Can Be Found Here: Parkmount Financial Investment Advisory Brochure

“Parkmount Financial Partners LLC” (herein “Parkmount Financial”) is a registered investment advisor offering advisory services in the State[s] of Massachusetts and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training.

The information on this site is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Parkmount Financial disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

Parkmount Financial does not warrant that the information on this site will be free from error. Your use of the information is at your sole risk. Under no circumstances shall Parkmount Financial be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided on this site, even if Parkmount Financial or a Parkmount Financial authorized representative has been advised of the possibility of such damages. Information contained on this site should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

Comments