Insurance Financial Advisor vs Fee-Only Financial Planner (Northwestern Mutual, New York Life, MassMutual Affiliated & Independent Advisors Compared)

- Joe Boughan

- Mar 1

- 7 min read

Many people go shopping online for and advisor and properly do their research.

But, believe it or not, most people don’t wake up and decide to “hire a financial advisor.”

They meet one.

A friend introduces them. A coworker makes a referral.

Someone says, “You should talk to my advisor — he works with Northwestern Mutual.”

That feels safe.

Recognizable brand. Established company. Professional presentation.

And that’s often where the relationship begins.

But here’s something most people don’t think about at the start:

The structure behind your advisor often influences how advice is delivered — even when the individual advisor is well-intentioned.

That’s not criticism. It’s reality.

If you’re comparing an insurance based advisor to other type models of advice you may be trying to compare Northwestern Mutual vs fee-only advisor, or wondering whether working with a New York Life financial advisor vs independent planner really makes a difference, this article is meant to slow things down and make the distinctions clearer.

There are also many other insurance based advisory firms like Mass Mutual which has independently branded but affiliated firms, or Penn Mutual which has similarly independently branded affiliated firms associated with them. Additionally, Guardian is another firm that is like Mass Mutual or Penn.

So, If you are researching for financial advice and options and this is a question on your mind, you can request a free consultation for a second opinion here:

No pressure. Just clarity.

Why Many People Start With Insurance-Based Advisors

Insurance firms are very good at building relationships and sales.

Referrals are encouraged. Networking is part of the culture. Many clients meet their advisor through someone they already trust.

That matters.

The issue isn’t trust.

The issue is that most people don’t initially ask:

How is my advisor compensated?

What incentives exist behind recommendations?

What will this relationship look like five years from now?

Those questions usually show up later.

Often after products are already in place.

I’ve had conversations with people years into a relationship who weren’t entirely sure how they were paying — or what alternatives might have existed at the beginning.

That doesn’t mean something was wrong.

It just means structure wasn’t fully understood.

Advice vs Product Distribution: The Structural Difference

Here’s the simplest way to think about it.

A fee-only independent advisor is typically compensated for ongoing planning and advice.

The National Association of Personal Financial Advisors has a very useful guide on what "fee only" means and typically looks like here:

An insurance-affiliated advisor is quite different from that structure. Typically insurance affiliated advisors are compensated when products are implemented, and sales of insurance are made, even if planning is part of that process.

That doesn’t automatically create a problem.

But incentives can shape emphasis in the relationship.

Compensation structures can potentially influence how solutions are presented and prioritized.

Insurance-affiliated advisors often have deeper familiarity with their firm’s product offerings, and their compensation may be finely tuned to how much of their firm's propriety products are sold in any given year.

By contrast, Independent advisors may have more flexibility to evaluate solutions across multiple providers with less pressure to promote one specific company's product over another for any given financial need.

No model can actually eliminates bias.

But the structure here is what matters.

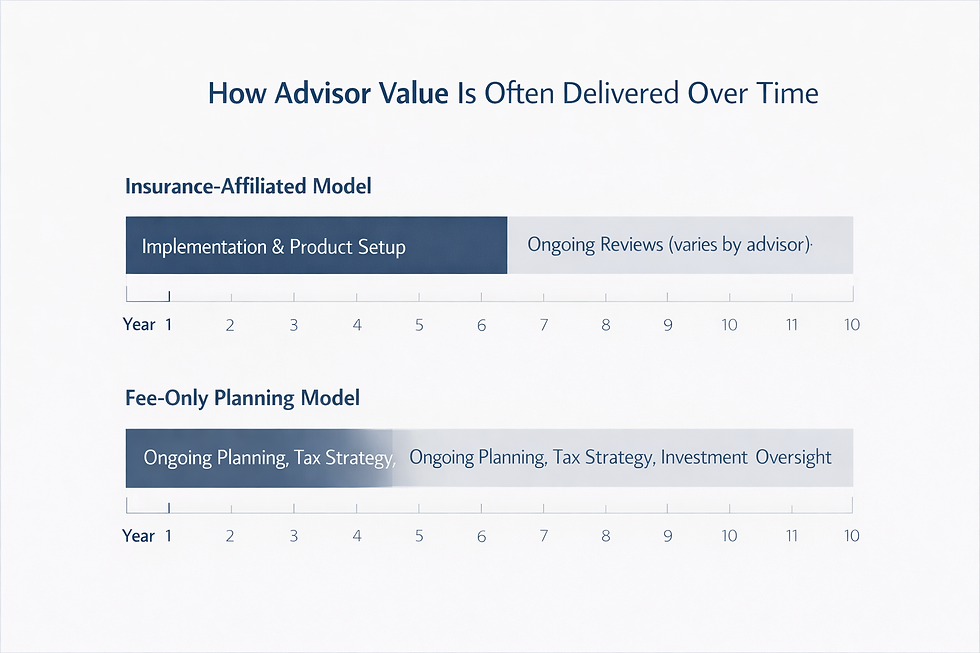

What Clients Often Notice Years Later

The biggest differences don’t usually show up in year one.

They show up in year four.

Insurance-based relationships can be very strong upfront. Implementation is focused. Education happens. Policies are placed. Accounts are opened.

Then life keeps moving.

Ongoing engagement varies from advisor to advisor. Some remain deeply involved. Others shift into a lighter periodic review rhythm.

Fee-only relationships can vary. Some are transactional but the most common type of model is like a subscription type engagement either through client paid fees or investment advisory fees. Since compensation to the advisor is set at a more ongoing rhythm, and not front loaded on commissions, the advisor has incentive to provide support that is more consistent and aiming for continuous planning value and experience:

Tax strategy

Retirement income modeling

Social Security decisions

Investment oversight

Healthcare planning

Behavioral coaching during volatility

The key difference is usually not intelligence or ethics.

It’s continuity.

Fee Transparency: Visible vs Embedded Costs

One of the most common comparison searches is:

“Northwestern Mutual vs independent advisor fees.”

The confusion here is understandable.

Certain insurance and brokerage products may include embedded costs or internal expenses that aren’t billed separately as advisory fees.

That can make the relationship feel inexpensive. Some people think there are no fees which may bias how they view alternatives.

Fee-only advisors typically bill transparently.

You see the number.

And psychologically, visible fees feel heavier than embedded ones.

Humans react more strongly to what they can see.

That doesn’t mean one approach is automatically more expensive. Costs vary widely.

It does mean clarity tends to be higher when fees are explicit.

And clarity reduces second-guessing later.

The cost may feel higher with a fee only advisor In many cases. My view is that if you have spent time developing a plan that covers a broad scope and advisor on the same side of the table as you when choosing investments, insurance products, or other financial planning techniques, you will likely get a return on the fees paid from the ability to make suggestions more aligned to your best interest. That can make a real financial difference in your life.

Conflicts of Interest: It’s About Magnitude, Not Morality

Every advisor operates within incentives.

The real question isn’t whether conflicts exist.

It’s how strong they are — and how visible they are.

Compensation structures can influence which solutions receive emphasis.

That’s true in every industry.

Fee-only advisors may have incentives tied to assets under management. Insurance-affiliated advisors may have incentives tied to product placement.

Neither system removes human bias.

But independence may allow evaluation of a broader range of solutions, depending on firm structure.

And that flexibility can matter in complex planning situations.

Fiduciary Status: A Nuanced but Important Distinction

Many people searching “Is Northwestern Mutual a fiduciary?” are really asking a deeper question:

Who is legally obligated to prioritize my interests — and when?

Many fee-only registered investment advisors operate under a fiduciary standard throughout the advisory relationship, though investors should confirm how that applies in their specific case.

Insurance and brokerage professionals may operate under different regulatory standards depending on the services provided.

Financial advice isn’t a one-time transaction. It unfolds over decades.

Understanding how fiduciary responsibility applies within your specific relationship is worth clarifying.

For additional context, these neutral resources are helpful:

CFP Board Code of Ethics:https://www.cfp.net/ethics/code-of-ethics-and-standards-of-conduct

Those explain the regulatory landscape and are truly great resources.

Flexibility When Life Changes

Financial plans look clean on paper.

Real life does not.

Careers shift. Parents need care. Businesses sell. Health changes. Markets don’t cooperate.

Some insurance-based solutions can be valuable tools.

But once implemented, adjustments can be more complex than simply changing an investment allocation.

Fee-only planning structures often remain more adaptable because they aren’t anchored to a single product decision.

Flexibility becomes most valuable precisely when life stops being predictable.

Which it eventually does.

The Questions I Hear Most Often

When people start comparing Insurance Employee financial advisor ( New York Life, Northwestern Mutual, etc. ) vs fee-only financial advisor, the questions tend to sound like this:

Do I clearly understand how my advisor is paid?

Is my strategy driven more by products or by planning?

Am I receiving proactive planning — or mainly reactive reviews?

Can my advisor recommend solutions outside their firm’s ecosystem?

If I asked for alternatives, would I receive them?

Switching advisors isn’t always necessary.

But understanding your structure clearly almost always is.

Final Thought

This isn’t about labeling one model good and another bad.

Some insurance-affiliated advisors provide excellent guidance.

Some fee-only advisors provide average guidance.

The more important issue is structural alignment.

Your advisor relationship influences retirement decisions, tax efficiency, emotional stability during volatility, and long-term confidence.

Choosing the right structure doesn’t guarantee outcomes.

But it does influence the environment in which decisions are made.

And that environment matters more than most people realize at the beginning.

If You’d Like a Second Perspective

If this article raised questions about your current strategy, that’s normal.

Many investors don’t fully understand advisor model differences until later in the relationship.

If you’d like a thoughtful, pressure-free second opinion:

Just a conversation. No obligation.

Disclosures Can Be Found Here: Parkmount Financial Investment Advisory Brochure

“Parkmount Financial Partners LLC” (herein “Parkmount Financial”) is a registered investment advisor offering advisory services in the State[s] of Massachusetts and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training.

The information on this site is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Parkmount Financial disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

Parkmount Financial does not warrant that the information on this site will be free from error. Your use of the information is at your sole risk. Under no circumstances shall Parkmount Financial be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided on this site, even if Parkmount Financial or a Parkmount Financial authorized representative has been advised of the possibility of such damages. Information contained on this site should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

Comments